Financer ses projets grâce aux aides

Comment le «gouvernement» a payé nos vacances soleil… ![]() Mon absence du dernier mois était plutôt justifiable quand même: je suis partie en vacances (et accessoirement je me suis mariée en même temps…)! Des vacances attendues et planifiées de longue date… et à force d’économies!

Mon absence du dernier mois était plutôt justifiable quand même: je suis partie en vacances (et accessoirement je me suis mariée en même temps…)! Des vacances attendues et planifiées de longue date… et à force d’économies!

Avez-vous essayé Tuango ?

Intéressé par le concept des rabais pour les groupes? En ce cas, vous devez (ou devriez?) connaître Tuango.

Faire faillite, c’est facile !

La perspective de faire faillite est-elle encore aujourd’hui source d’angoisse? Pas pour tout le monde.

Défi de Février, saurez-vous battre votre score de Janvier ?

Bonsoir à tous!

Alors ce soir, bilan du défi de janvier… vos journées dépenses zéro, vous finissez à combien? Pour ma part, je termine à 19 journées… non consécutives bien sûr!

Payez vos dettes !

Ceux qui suivent l’actualité financière ont noté cet été que la Réserve fédérale américaine est revenue sur sa décision de monter les taux d’intérêt, et ce probablement jusque vers 2013.

Types of Annuities and How they Work

The other day I was craving tacos. The hunger was fierce. So, I decided to head to my favorite Mexican restaurant to satisfy my appetite.

Usually, I choose between either coconut shrimp or carnitas. But, on this particular day, I wanted to try something different. But, I quickly became overwhelmed by the possibilities.

Granted, this was a Chiptole situation where I could apparently have some 655,360 combinations to pick from.But, stilll, the decision wasn’t easy. And, while I was standing in line, I got to thinking. This is kinda similar to annuities.

That might seem like a stretch. But, it’s true. If you want to buy a taco, you have several different options based on your preferences and dietary needs. The same is true with annuities. There are different types that are designed to meet your specific retirement needs.

So, let’s explore what the different types of annuities are and how they work so that you can pick the best one.

The Main Types of Annuities

Generally speaking, there are two basic annuity types, immediate and deferred. The main difference between them is your payout options. With an immediate annuity, you’ll receive payments right away. A deferred annuity will have to wait until a future date to collect your money.

Here’s where things can get hairy. Within these basic categories there are three other types of annuities;

- Fixed. As a result of the contract, you will receive a fixed amount based on an interest rate.

- Variable. This is a tax-deferred annuity that allows you to invest finances into subaccounts.

- Indexed. The return is based on the performance of a stock index, such as the S&P 500 Composite Stock Price Index.

Still, confused? No worries. Let’s further explain what these annuity types are and how they operate.

Fixed

The least risky, most predictable, and straightforward annuity option available. With fixed annuities, the rate of interest is guaranteed and doesn’t change once the contract has been signed. For example, with a Due Fixed Annuity, you’ll receive 3% on every dollar deposited.

However, there are some fixed annuities that where the rate will rise and fall. Often, an interest rate reset occurs after a specified period of time.

In short, a mixed annuity performs like a certificate of deposit (CD). Like a CD, a fixed annuity offers principal protection. As such, it’s a low-risk investment. That does come at the expense of higher growth potential. Upon maturity, you can collect your funds at a guaranteed minimum rate.

However, that’s where the similarities end. In most cases, CDs are used for short-term goals, like putting down a down payment on a house. On the other hand, fixed annuities are long-term investments that you’ll wait and use when in retirement.

How does a fixed annuity work?

An insurance or annuity company sells you a fixed annuity. You have the option to pay this in installments or a lump sum payment. In return, you receive a certain interest rate that the company guarantees.

It’s during the accumulation phase where tax-deferred growth takes place. And, how much you’ll get is determined by the following factors;

- Amount of the premium

- The current interest rate

- How old are you and how long do you expect to live

- Your gender

Or, you could save yourself the trouble and just stick with a fixed annuity that’s transparent from the get-go. Hint: this would be Due and it’s 3% guaranteed interest rate.

Variable

As with a fixed annuity, a variable annuity is a contract between you and an insurance/annuity company. But, it also grows on a tax-deferred basis and provides a guaranteed retirement income stream. And, it can be purchased with either a single payment or a series of multiple payments.

The key difference? With a variable annuity, you choose from a wide range of investment options known as sub-accounts. As a consequence, this will vary the value of your annuity contract.

Unlike a fixed annuity, the value of your contract fluctuates. This is determined by how your investments are fairing. In most cases, your investment options are mutual funds comprised of stocks, bonds, and, and money market instruments. Often, this will be a combination of these investments.

That means that the potential growth is higher with a variable annuity than a fixed annuity. However, you could also lose money with a variable annuity making it a riskier option. You can attach riders, which you’ll you have to pay for, that can help protect you against market losses.

Because variable annuities hold unique benefits that aren’t available in other insurance products or investment options, they’re distinct. Just note that this uniqueness does come with a price in the form of expensive annuity fees.

How does a variable annuity work?

Purchasing a variable annuity does not mean that you’ll be in the dark regarding your available investment options. There are generally three types of mutual funds when you purchase a variable annuity; stock, bond, and money market. Additionally, you may be able to select other investments, such as stable income value mutual funds.

You don’t have to worry about the accumulation period if you choose an immediate variable annuity. This is because you’ll begin receiving payments as early as a year from buying the contract.

Deferred variable annuities do not follow the same rule though. There are two phases if you select this option, a phase of accumulation followed by a phase of payout. In short, this means you’ll get your money sometime down the road.

Indexed

Also known as equity-indexed annuities or fixed-indexed annuities, index annuities combine the best features both of fixed and variable annuities. But, it also stands on its own by offering unique features. This includes providing a minimum guaranteed interest rate in addition to an interest rate that’s linked to a market index.

Annuities are generally based on well-known and broad indexes. Standard & Poor’s index of 500 stocks is the most popular. Some annuity contracts, however, are based on other indexes like the Nasdaq 100, the Russell 2000, and the Euro Stoxx 50.

In addition, some of these indices may represent certain market segments, while others may allow investors to pick multiple indexes. Moreover, you’ll have more risk, but less growth potential than you would with a fixed annuity thanks to the guaranteed interest rate. However, they’re not as risky or as high-yielding as variable annuities.

How does an indexed annuity work?

Owners of indexed annuities are more likely to earn higher returns than owners of other annuity types. It’s clear that indexed annuities only provide a better return than fixed annuities when the markets are performing well. Additionally, they do provide some level of protection against market declines making them less risky than variable annuities.

As with other annuity types, you promised a guaranteed income stream that grows tax-deferred. Also, you can fund an indexed annuity with one lump sum or recurring payments over time. But, you can decide when you want withdrawals to begin.

When you go to buy an indexed annuity contract, you’ll select an index, such as the S&P 500. The annuity company invests this money into that specific index. However, never put all of your eggs into one basket. As such, you should diversify your portfolio by placing your money into various indexes.

How is the rate on an indexed annuity is calculated? You select an index that reflects the change over the previous year. Alternatively, it may be based on a 12-month average gain. Overall, a specific index is used to index annuities.

There is a major concern with indexed annuities though. And, that’s that you may not receive the full benefits of index rises. The reason? There may be limits on potential gains. This is commonly known as the “participation rate.” If the participation rate is 100%, your account will be credited with all of the gains. The percentage may be as low as 25%, however. Usually, indexed annuities offer at least 80% to 90% participation rates.

Annuity Payout Options

In case you forget, annuities can be either immediate or deferred. What separates these two types is when you’ll begin receiving payments..

Immediate Annuity

An immediate annuity pays out payments within a year after it is purchased and is sometimes called an income annuity. An example of this might be winning the lottery or receiving an inheritance. Or, maybe you have a large sum of money stashed away.

Regardless, you purchase an immediate annuity with one payment. From there, you’ll receive guaranteed payments either for life or a specific timeframe. This is better suited for people approaching or already in retirement.

Why would people buy an immediate annuity? Well, it can prevent them from spending this large lump sum of cash. And, it’s also an effective way to supplement other retirement income, such as Social Security.

Deferred Annuity

With a deferred annuity, investors receive future payments. In most cases, this happens when an investor retires. During this time, the investment grows tax-deferred.

Deferred annuities are a better option for younger investors who have the time to let their savings accumulate. The downside? If you do need this money prior to age 59 ½, you’ll get slapped by a 10% IRS penalty fee.

How Long Are Annuities Paid?

Annuities generally provide longevity protection. That means annuities offer lifetime income that the owner can not outlive. But, there are a variety of options you can pick from.

Lifetime Annuities

These are guaranteed income streams during the annuitant’s lifetime. Some lifetime annuities do allow for beneficiaries to continue receiving payments after the annuitant dies. Annuity payments are based on the health and age of the annuitant.

Fixed-Period Annuities

An annuity with a fixed period, which is also called a term-certain annuity, is like winning a lottery prize. You can either take the cash amount now or receive payments that take place over a number of overs. Typically, payments are spread out over a 20- or 30-year period. A perk with this type of annuity is that it doesn’t take into account the age or health of the annuitant.

Are There Any Other Annuity Options?

To complicate matters even more, there are the following annuity options depending on if you have benfiaricies or not.

- Annuities that pay only for the duration of the annuitant’s life are called life-only annuities. It’s possible to include provisions for your spouse or even a refund.

- Period certain life annuities continue to pay even if the annuitant dies before the end of the period.

- In the case of joint and survivorship annuities, the annuitant and a beneficiary both receive payments over their lives.

And, one more thing. Annuities can be either qualified or non-qualified.

“A qualified annuity is funded by pre-tax dollars,” states Deanna Ritchie in a previous Due article. “Contributions to a qualified annuity are dependent on your income. Therefore, you must also follow the required minimum distribution rules that are also applied to traditional 401(k)s and IRAs. This means that you must begin taking minimum distributions starting at the age of 70 ½.”

“With non-qualified annuities, you’re using after-tax dollars to fund the annuity,” adds Albert Costill in yet another Due piece. “That means you’ve already paid taxes on the money that you used to purchase it with.”

“Additionally, there are no required minimum distributions,” he says. “So, in a way, this is similar to how a Roth individual retirement account works. Unlike a Roth IRA, however, earnings that are withdrawn from non-qualified annuities are taxable at your regular tax rate.”

“And, the IRS doesn’t impose limitations on how much you can contribute to a non-qualified annuity annually. Just be aware that the insurance company that sold you the annuity may set an annual cap on contributions.”

Which Annuity Should You Buy?

Before committing to any annuity type, reflect on your specific goals and needs. You should also take stock of your risk level. And, you could also ask the following questions;

- Is your goal long-term growth or a guaranteed income?

- When are you planning to retire?

- Do you have any other sources of income?

- Do you have a plan for potential lifestyle changes and steady income loss?

For example, a fixed annuity might be your best bet if you hope for a reliable, lifetime income with low risk and costs attached. A variable annuity is worth exploring if you’re willing to take the risk of obtaining higher returns.

Additionally, you can add riders to customize the contract to suit your needs, such as long-term care insurance. As an example, leaving your loved ones a legacy. If so, consider adding a rider that permits you to designate beneficiaries.

Ultimately, you want to talk to a trusted finanical professional before buying any type of annuity. They can help you decide on which option is best for you and your financial future.

Best Annuity Rates to Help Your Money Grow Everyday

Annuity rates are the percentage your annuity grows each and every year. Whether you’re still in the planning stages or have just recently retired, you’re probably concerned about being able to cover your living, healthcare, and medical expenses. You’ve also probably had many sleepless nights worrying whether you’re going to outlive your savings or not. While all retirement concerns are valid, there might be a rare one-fix solution to put your mind at ease. And, it’s through an annuity. The key is finding the right annuity for you. Here are the best annuity rates on the market.

Annuities are insurance contracts. They provide a guaranteed lifetime income and protection against losing your initial investment. You may be able to use an annuity to assist you with your long-term costs too. And, you can leave the balance to heirs.

Unfortunately, many people aren’t taking advantage of annuities. Maybe it’s because they’re overwhelmed by them — or overwhelmed by all things about retirement. And, that’s a fair point. After all, annuities come in a variety of flavors — just like ice cream.

For starters, an annuity rates can be either immediate (begin paying out now) or deferred (being paying out at a later date). Additionally, they might fall into the following annuity types;

- Fixed annuities promise to pay you a guaranteed interest on your contributions. Rates are often based on the current interest environment. Overall, a fixed annuity is the most straightforward and predictable.

- Fixed indexed income annuities also offer principal protection like a traditional fixed annuity. However, there is upside potential through index participation (such as S&P 500). Principal protection and growth.

- Multi-year guaranteed annuities (MYGA) offer a fixed rate of return, but for a specified period of time.

- Variable annuities are tied to an investment portfolio. So, payments can increase when the market is performing well and decrease when it’s not. You can expect higher returns, but there’s more risk involved.

- Registered index-linked annuities are relatively new and are tied to the stock market index. Gains are capped and losses are limited.

What to look for when buying an annuity?

Are you feeling comfortable enough with annuities now that you want to buy one? If so, you’ll want to keep the following in mind so that you’ll get the most out of the annuity.

Pick the right type of annuity for you.

If you’re allergic to peanuts, then you should stay far away from peanut butter ice cream. It’s kind of the same thing with annuities. If you’re already in retirement, then a deferred variable annuity probably doesn’t make much sense. Select the annuity that best aligns with your retirement plan and doesn’t exceed your risk threshold.

Check the annuity rates and terms.

Before committing to a contract, carefully review the rates and terms. It should be clearly stated when you can access your money, how much you’ll be receiving, and the fees associated with the annuity. For example, if you withdraw any money before you’re permitted, you’ll be subject to surrender charges.

Choose your salesperson wisely.

Since your broker has to put food on the table, they’ll earn a commission from annuity sales. Often, these costs aren’t disclosed. Find out how much they’re making off the sale. And, more importantly, that they’re not selling the wrong annuity just to cash in on a commission.

Select a financially strong insurance company.

Annuities aren’t backed by institutions like the FDIC. They’re also supposed to last you a lifetime. As such, you need to make sure that you’re working with an insurance company that’s in it for the long haul. You can make sure that they’ve received a high rating from third parties like A.M. Best, Moody’s, Standard & Poor’s (S&P), and/or Fitch, etc.

Some other considerations? How easy it is to sign up and fund the annuity, as well as access your money. Customer service and what you expect your payments to be should also be factored in. Also, look at the interest rates for payout.

But, since your time is valuable, we’ve gone ahead and listed the 25 best annuities that you should purchase. Each has met the criteria above. And, we’ve even broken the list down into the best fixed, fixed indexed growth, MYGA, variable, and registered index-linked annuities so that you can quickly find the right type of annuity for you.

Top Annuity Rates

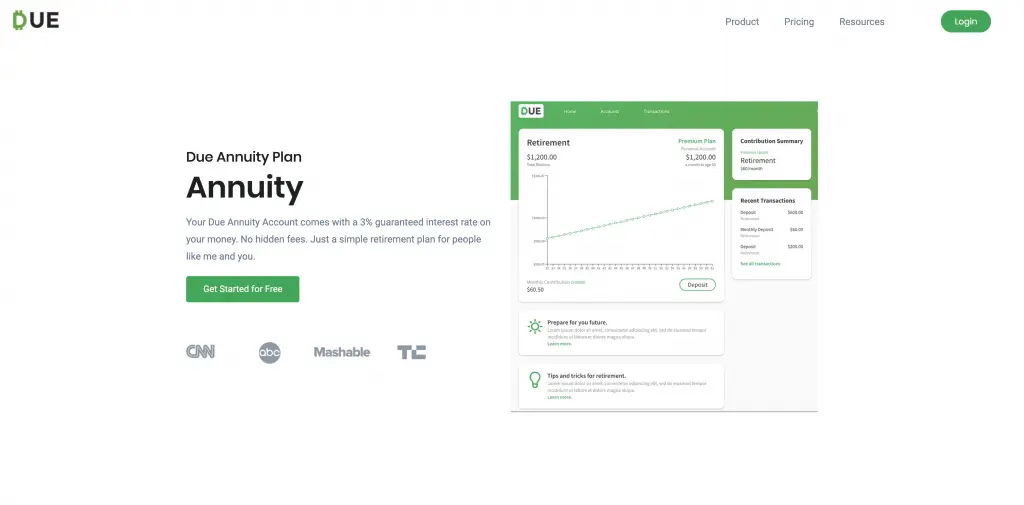

1. Due Fixed Annuity

When it comes to fixed annuities, Due has quickly established itself as a market leader. Founded by entrepreneur serial and annuity expert John Rampton, the company has already secured over 12,000 registered users. Those who sign up for a Due account can anticipate a guaranteed annuity rate of 3% return. And, on average, users are receiving $2,100 in retirement income per month.

But what makes Due the nation’s top retirement app? Easy. It’s incredibly accessible and easy to understand.

Due was designed for the average person to finally grab a piece of that guaranteed income ice cream cake. As such, it’s one of the most straightforward and transparent annuities on the market. And, here’s how it works.

Just apply for a Due account. Don’t worry. It’s free and will take you under 10-minutes. Once you’re set-up, you’ll get 3% on every dollar deposited.

That’s it. No frills. No BS.

And, if you’re uncertain on how much you’ll need to save each month, there’s also a handy annuity calculator to determine this amount. And, all of your hard money is deposited into a Charles Schwab account. It’s then managed by Blackstone (NYSE: BX), and ATHOS Private Wealth. If you’re unaware, both have impeccable reputations as two of the best investment firms in the country.

2. American National Single Premium Immediate Annuity (SPIA)

Since 1905, American National has been providing insurance products and services, including annuities. The company has three annuity options; a fixed deferred annuity, index deferred annuity and an SPIA.

Because American National has an A rating from A.M. Best you can be certain that the company is financially strong and will be sticking around. That makes all of their offerings appealing. But, their SPIA is the superstar of the bunch.

With this annuity, you can convert a lump sum of money into a predictable income stream. In fact, a “joint life” option has an average annual income of $10,609 and an annual payout rate of 5.30% — but it changes with what the current percentages are at the time of payout. You can spread this income out over a number of years, making your taxes more manageable, and there are several cash-out options. That makes it easier to withdraw your money in case there’s an emergency — but as with all annuities, there are fees with early withdrawal.

3. CUNA Mutual Group MaxProtect Fixed Annuity

Issued by the CMFG Life Insurance Company, the MaxProtect Fixed Annuity offers a guaranteed and competitive rate. That means you don’t have to sweat market volatility. But, at the same time, your annuity will grow faster than other taxable investments like CDs.

CUNA also gives you the option to lock in your interest rate for 3, 5 or 7 years. Afterward, you have several options to turn your savings into a series of income payments. And, there are no contract, administrative or upfront fees.

A.M. Best rated CUNA “A,” Standard & Poor’s (S&P) gave it an “A+” and Moody’s gave it an “A2.” That means you should have no concerns over CUNA’s financial future.

4. New York Life Secure Term Choice Fixed Annuity II

In general, you can’t go wrong with any New York Life annuity. After all, the company has a long and rich history dating back to 1845. It also has an A++ from A.M. Best, and has been the top provider of fixed deferred annuities since 2010. The company has also received the highest score among individual annuity providers in customer service by J.D. Power.

But, we’ve selected the New York Life Secure Term Choice Fixed Annuity II as our favorite annuity offering from the company. It requires a $5,000 premium amount to begin, but there aren’t any annual charges. Annuity rates are subject to and depend on the length of the contract, but the Guaranteed Minimum Interest Rate (GMIR) is 0.05% (except in New York where it is 1%). And, you also have the option to go with a 3, 4, 5, 6, or 7-year policy.

5. American Equity GuaranteeShield

Online reviews for American Equity have noted that American Equity delivers outstanding customer service. And, as far as financial strength goes, it’s earned an A- (Excellent) from A.M. Best. Furthermore, the company has several different annuity options.

For our money, though, we like the GuaranteeShield series. It checks all the boxes for a fixed annuity, including;

- Principal protection

- Guaranteed income

- Tax-deferred growth

- Liquidity

- May avoid probate

You can also access up to 10% of your contract’s value each year and add on a market value adjustment and death benefit rider. Interest rates may vary each contract year. But, the GMIR will never drop below 1%.

Top Fixed Indexed Growth Annuities

6. AIG – Assured Edge Income Builder

With the Assured Edge Income Builder from AIG, you can reap the benefits of a fixed annuity. Additionally, your guaranteed lifetime income amount (GLIA) will increase based on a 7% income growth rate each year until you begin receiving payments. And, according to the company, the annual income credit is a dollar amount calculated by multiplying the initial GLIA by the 7% income growth rate.

But, there are a couple of other features that make this a highly coveted annuity. There’s also a market value adjustment and a flexible guaranteed withdrawal benefit (GLWB). For example, being able to take multiple withdrawals of up to 10% of your contract value as of the previous anniversary, with no withdrawal charge or market value adjustment (MVA).

You’ll need a $25,000 minimum deposit. And, you should also know that AIG has received an A from A.M. Best, A2 from Moody’s, A+ from S&P, and A+ from Fitch.

7. Nationwide – New Heights 9

Going back to 1926, Nationwide offers insurance, retirement, and annuity products. What makes Nationwide a top annuity company is that its products are flexible. For example, you can purchase a premium through a series of payments or just one lump sum.

In particular, the company’s New Heights 9 Fixed Indexed Annuity deserves a shoutout. As stated on the company’s site, “New Heights 9 tracks your potential strategy earnings also known as earnings, daily, and does not limit the amount of index performance used to calculate your earnings.” You also might be able to snag higher long-term accumulation depending on the performance of the underlying index and declared percentage or rate component.

Additionally, your money is protected from potential market risk. And, you can also tack on optional riders. One such rider worth considering is guaranteeing a lifetime income for you, your spouse, or heirs.

Additionally, Nationwide has landed high financial ratings. A.M. Best rated it an A+ (Superior), S&P gave it an A+ (Extremely Strong), and Moody’s rated it an A1 (Upper-Medium Grade).

8. Protective Indexed Annuity II

Protective has been in business since 1907. And, throughout the years they’ve garnered an A+ rating from A.M. Best, AA- from S&P, A1 from Moody’s, and A+ from Fitch. They also just so happen to be one of the top-selling registered-index-linked companies.

With that in mind, we would be remiss if we didn’t mention its Indexed Annuity II. The company promises protection on your principal, a lifetime stream of guaranteed income, and potential for higher growth based on the performance of the S&P 500 Index. One of the most appealing features, however, is that you’re able to access your money penalty-free if you become unemployed, terminally ill, or have to relocate to a nursing facility.

There’s a $10,000 minimum. But, you don’t have to be concerned with an annual contract fee.

9. Global Atlantic ForeIncome II

Global Atlantic offers several different annuity products including a fixed, variable, income, or fixed index annuity. And, it’s the latter that we want to focus on.

It turns out the Global Atlantic has five different fixed index annuities, FIAs for short. The purpose of these is that you’ll have greater growth potential than traditional deposit products, tax-deferred growth, and no market losses. Also, you can pass the balance on to your beneficiaries.

Specifically, the ForeIncome II stands out the most. It aims to provide you with a “retirement paycheck” for life. And, this is an extra income that you can’t outlive. What’s more, you have two withdrawal options;

- The Guaranteed Income Builder Benefit offers a steady, predictable income for your entire life.

- The Income Multiplier Benefit provides a steady income, but it grows by being tied to the S&P 500.

And, there’s no need to stress over Global Atlantic’s financial strength. The company has earned an A from A.M. Best, Fitch, and Moody’s, along with an A- from Standard & Poor’s.

10. Lincoln Financial OptiBlend

Lincoln Financial has been in existence since 1905. The company offers a wide range of products including annuities, life insurance, retirement plan services, and group protection. But, obviously, we want to highlight the company’s annuities — specifically the Lincoln OptiBlend.

This is a fixed indexed annuity. It has flexible premium annuities and offers a set interest rate for one year. Interest rates are declared annually. Another key feature includes a 5-year, 7-year or 10-year surrender charge schedule.

But, the standout is that your portfolio is tied to the performance of four different indexed accounts; the 1 Year Fidelity AIM Dividend Participation, 1 Year S&P 500 5% Daily Risk Control Spread, 1 Year S&P 500 Cap, and 1 Year S&P 500 Participation.

There’s a $10,000 minimum. But, no annual contract fees.

Top Multi-year Guaranteed Annuities

Before we can go any further, you must know that these rates change frequently. As such, the rates we’re including here are from June 2021. To check the most up-to-date rates, visit a source like Blueprint Income or the Annuity Guys.

11. Sentinel Security Life

This Utah-based business has been in operation since 1948. And, like insurers, they offer multiple annuity products including a fixed indexed and income annuity. However, the company offers some of the highest MYGAs annuity rates on the market.

Case in point, if you purchase a 10-year term, you’ll receive up to 3.20%. You’ll most likely need a $2,500 minimum initial premium — if you opt for Sentinel Security Life’s Personal Choice annuity. And, there aren’t any contract fees. We’re also like that if you become terminally ill or nursing home care withdrawal charges are waived.

What about Sentinel’s financial strength? A.M. Best ranked the firm at a B++ (Good). If you’re curious, this rating comes in eighth on A.M. Best’s scale of 21 possible grades.

12. Atlantic Coast Life Insurance

Founded in 1925, Atlantic Coast Life Insurance is based out of Charleston, SC. While the company may not be a household name, it also offers favorable MYGA rates. One of its best is its 20-year term annuity that will fetch up to 3.30%.

Just for comparison’s sake, CDs offered online are paying 3% or less on a five-year paper. And, CDs available at bank branches are substantially less than this. So, we’ll take that 3.30%.

If you’re wary about Atlantic Coast Life Insurance it was rated a healthy B++ by A.M. Best. And, you may even land a first-year bonus of an additional one percentage point.

13. Canvas Annuity Future Fund

Canvas is built around being a people-first annuity company. It promises great rates, flexible access, and absolutely zero commissions. In short, the company states that its revolutionizing annuities.

Considering that Canvas has a guaranteed crediting rate for the following term, 7 years and it’s annuity rates are up to 3.25%, you can’t argue with that sentiment. Moreover, you have 24/7 access to your information online and it’s available for anyone aged 18-90 years old. You’ll just need a $2,500 minimum initial premium.

The Scottsdale, AZ company has a B++ rating from A.M. Best. And, its annuities are issued by Puritan Life Insurance Company of America.

14. Oceanview Life Harbourview MYGAs

A.M. Best has rated Oceanview an “A-”. Which means the company has a stable outlook. What’s more, the company had multiple interest guarantee periods — 3, 4, 5, 6, 7 & 10 Years. But, what’s interesting is that the issue age is 0 through 89.

But, the company also has competitive rates, such as its 10-year term and annuity rate up to 3.10%. You’ll need a $20,000 premium requirement and there is a market value adjustment. And, the company also offers 10% free withdrawals.

15. Nassau Simple Annuity

Based in Hartford, CT, Nassau Financial Group covers insurance, reinsurance, distribution and asset management. However, you probably can’t go wrong with its 6-year term where you’ll earn up to 3.10%.

Overall, this is a single-premium, multi-year guaranteed annuity that offers protection from market volatility. The premium range is between $5,000 – $1,00,000. Also, the issue age is 18-85.

The company’s financial strength is solid as it has received a B+ from A.M. Best.

Top Variable Annuities

16. Fidelity Personal Retirement Annuity

Fidelity offers six quality annuities. And, it’s this variety, along with the company’s reputation for delivering stellar customer service, that makes it stand out. But, we’re fans of the Fidelity Personal Retirement Annuity.

Considered a top variable annuity by Barron’s this is a low-cost, tax-deferred annuity that gives you three different investment approaches, as described by the company;

- A hands-off approach might be a fit if you don’t want to actively manage your portfolio and prefer to choose one single fund where Fidelity provides automatic diversification and professional money management.

- A hands-on approach might be a fit if you want to manage your own investments. You’ll be able to utilize our powerful research tools to choose from more than 55 Fidelity and non-Fidelity funds, many rated 4 or 5 stars by Morningstar.

- A sector investing approach might be a fit if you are interested in managing your own investments while focusing on 11 funds that each represent a specific segment of the economy.

A minimum investment of $10,000 is required. But, the annual annuity fees are some of the lowest in the industry — 0.25% for contracts purchased with an initial investment of less than $1 million.

17. Jackson National Life Perspective II

Even though Jackson National Life is a subsidiary of the British insurer, Prudential plc., its origins go back to 1961 in Jackson, Michigan. Over the years, the company has earned a solid reputation for its financial strength. In fact, Jackson National Life Insurance has received an A (Excellent) rating from AM Best.

The company offers fixed fixed index, and variable annuities. And, it’s its variable annuities that we want to shine a spotlight on. In particular, it’s the Perspective II contract.

It requires a minimum initial premium of $5,000 and has a $35 annual contract charge. You should also expect additional fees like a 1.30% core contract charge and 0.53% – 2.41% annual portfolio operating expenses.

Despite these fees, this annuity is designed for long-term investors with a timeframe of seven or more years. Most appealing is that you can attach the LifeGuard Freedom Flex. In a nutshell, this is Jackson’s version of the income rider benefit with an annual bonus guarantee of 7%. There’s also the opportunity to leave a legacy. And, you can view data for each of its variable annuity products through a partnership with Morningstar.

Finally, Jackson National Life is financially strong as it received an A (Excellent) rating from AM Best.

18. Transamerica Life Principium IV

Transamerica is one of the industry’s leading firms. The company has been around since 1928 and shows no signs of slowing down. After all, it’s securely landed within the top quarter of the A.M. Best, Moody’s, S&P Global, and Fitch scoring structures.

While the company does offer a variety of annuities, we’re partial to Principium IV. Fun fact. The word Principium comes from Latin to signify origin or root. The word itself, however, means principle — especially a basic one.

Overall, this is a lower-cost variable annuity containing a five-year surrender charge schedule. Other key features include automatic asset rebalancing, free transfers between subaccounts, and the ability for annuitization after the third policy anniversary. There’s also a dollar-cost averaging feature that will purchase more units when prices are low and fewer when prices are high.

A minimum initial premium of $1,000 is required if qualified and $5,000 for unqualified. There’s also a $35 annual service charge.

19. MassMutual Transitions Select II

MassMutual is known for providing a plethora of investment options for its variable annuity owners. And, each offering has varying philosophies and risk tolerance levels. As such, you might be able to find a product that fits you like a tailored suit.

If you want investment to be at the core of your variable annuity, then your best option is the Transitions Select II product. You can choose sub accounts that are managed by some of the industry’s heaviest hitters including Oppenheimer Funds, Fidelity, Black Rock, and Franklin Templeton Investments.

There are also flexible payment arrangements after five years and free withdrawals that are up to 10% of purchase payments. You can also sign-up for MassMutual’s free automatic investment plan (AIP) and automatic rebalancing program.

An initial investment of $3,000 (qualified), $5,000 (non-qualified), is required. There’s also a $40 annual contract maintenance fee. And, if you’re curious about its financial ratings, here’s what MassMutual has received:

- Fitch: AA+ (the second-highest of 21 grades)

- A.M. Best: A++ (the highest category of 15)

- Moody’s: Aa3 (fourth-highest of 21)

- Standard & Poor’s ranks it at an AA+ (second-highest of 21)

20. Brighthouse Financial Variable Annuities with FlexChoice Access

A variable annuity from Brighthouse, which has received an A rating from A.M. Best and Fitch, as well as an A+ from Standard & Poor’s, has the standard features you’d want. These include a guaranteed lifetime income and flexible investment options based on your personalized investment strategy. You can also set it up so that your spouse will continue to receive your payments.

But, it’s the FlexChoice option that makes this annuity worthy of inclusion. For starters, you’ll receive 5% annual compounding for the first 10 years of your contract. There’s also the ability to automatically lock in market gains and take either 6% or 4.75% withdrawals at age 65.

There’s a $10,000 minimum initial premium and a $30 annual contract fee. You should also expect additional fees, such as a 0.53% – 1.67% fund expense fee and 1.30% mortality/ expense/administration charge.

Top Registered Indexed Annuities

21. Athene Amplify

Like a Phoenix emerging from a financial crisis, since launching in 2009, Athene has quickly become an annuity market leader. In particular, its Amplify product is a shining star.

This is a 6-year registered index-linked annuity that allows you to pursue growth opportunities so that you’ll get the most out of your annuity without taking on too much risk. There’s also a lot of flexibility with this annuity. For starters, Amplify offers 1, 2 and 6-year term periods. There’s also 4 different index options. And, you can also leave a legacy.

In regards to its financial strength, Athene has scored an “A” from A.M. Best, Fitch, and S&P.

22. Equitable Structured Capital Strategies

Equitable Holdings Inc. was founded back in 1859. And, because of its financial strength, you can be confident that the company will be around for the foreseeable future. It has received an A from A.M. Best, A2 from Moody’s, and A+ from Standard & Poor’s.

As for annuities, we can get behind its Structured Capital Strategies variable annuity. Mainly because, as stated on its website, it “adapts to your unique investment styles so you can work toward your individual retirement goals on your terms.”

Specifically, this annuity provides the following;

- Levels of downside protection that are up to -30%

- Participation in indices, like the S&P 500 and Russell 2000, with the ability to up to a set performance cap rate, while also limiting your potential loss

- Customization, such as the maturity date (1, 3, or 5 years), how much you’re willing to risk, and the index you’d like to base the performance of your investment

You’ll need $25,000 to get started. And, there will be fees like a 1.65% variable investment option fee and 0.58% – 0.71% annual portfolio operating expenses.

23. Allianz Index Advantage

This is the company’s core index variable annuity. It’s “designed to help you accumulate money for retirement and provide income after you retire,” Allianz states on its website. “It can give you long-term growth potential through market participation – plus a level of protection – through a combination of traditional variable options and multiple index strategies.”

However, this annuity really shines because you can subscribe to a specific type of index strategy through the company. That’s a stark contrast to other annuities where the portfolio is constructed with securities, indexes, and investment strategies.

Note that there are two separate annual fees associated with the Allianz Index Advantage Variable Annuity. The first is a 1.25% product fee, as well as a 0.64% to 0.72% variable option fee. But, if you annex the optional death benefit plan for an additional 0.20% fee will join it.

Also, don’t forget about the $10,000 minimum initial premium. And, if you’re a curious cat, Allianz has a solid A+ AM Best Rating.

24. Nationwide Monument Advisor

Nationwide, and its superior A+ rating from A.M. Best, offers the industry’s first flat fee, Investment Only Variable Annuity (IOVA). As such, there’s a low-cost $20 per month flat fee. How far will that get you? Well, this annuity has over 350 investment options — which is the largest in the industry.

As such, this annuity is ideal if you’re looking for a low-cost option and/or investment diversification. In fact, it’s these two features that make the Nationwide Monument Advisor so engaging.

Just take note that you may have to pay other fees as well. For example, additional fund platform fees can range from 10% to 35%. So, if you’re not careful, this low-cost, tax-deferred annuity could become rather expensive. And, a $15,000 minimum deposit is also needed.

25. Prudential FlexGuard Indexed Variable Annuity

And, finally, we have the FlexGuard Indexed Variable Annuity from Prudential. This Fortune 500 company, which has an A+ from A.M. Best, states that this annuity can simplify your retirement planning while avoiding exposure to markets. It can also produce a reliable, “pension-like” guaranteed income stream.

FlexGuard also allows you to choose your buffer level as well as your term length and to allocate your money. This will be through well-known indices like S& P 500, iShares Russell 2000 ETF, Invesco QQQ ETF, and MSCI EAFE. And, perhaps most tempting, is that you can also select your own growth opportunity based on three different index returns; Point-to-Point with Cap Rate index, Tiered Participation Rate index strategy, or Step-Rate Plus.

You’re permitted to withdraw up to 10% of all purchase payments each year without incurring any surrender charges — just as long as the withdrawal is made within the surrender charge period. Other contract charges include Mortality, Expense, and Administration charges of 1.30% (M&E&A). These apply only when you allocate money to variable sub-accounts. And, a minimum purchase payment of $25,000 is required.

Here’s a summary of the best annuity rates of 2021

| Annuity Name | Type of Annuity | Deferred or Immediate? | Key Feature | Minimum Initial Premium | Guaranteed Rate of Return | Contract Term | Withdraw? | Annual Fees | A.M. Best Rating |

| Due Fixed Annuity | Fixed | Both | Accessibility. Anyone can apply in under 10 minutes. | $0.00 | 3.00% | – | Withdraw at anytime, Free – up to 10% of contract value | $10/month | – |

| American National Single Premium Immediate Annuity (SPIA) | Fixed | Immediate | Flexibility, like multiple income payment options. | $0.00 | 5.30% | – | Partial | None | A |

| CUNA Mutual Group MaxProtect Fixed Annuity | Fixed | Both | A market value adjustment and book value version | $10,000.00 | – | 3, 5, or 7 years | Free for health hardship | None | A |

| New York Life Secure Term Choice Fixed Annuity II | Fixed | Deferred | A market value adjustment that could boost your finances | $5,000.00 | 0.05% | 3, 4, 5, 6, or 7 years | Free – up to 10% of contract value | None | A++ |

| American Equity GuaranteeShield | Fixed | Deferred | Principal protection and guaranteed lifetime income | $10,000.00 | Never below 1% | 5, 6, or 7 years | Free – up to 10% of contract value | None | A- |

| AIG – Assured Edge Income Builder | Fixed Indexed Growth | Both | You can decide when payments will begin | $25,000.00 | 7.00% | 7 years | Multiple – up to 10% | None | A |

| Nationwide New Heights 9 | Fixed Indexed Growth | Deferred | Principal protection with higher long-term accumulation | $25,000.00 | 2%-5% | 9 years | Free – 7% of the contract’s value on the first day of the contract year | None | A+ |

| Protective Indexed Annuity II | Fixed Indexed Growth | Deferred | Can access money penalty-free if unemployed, terminally ill, or have to relocate to a nursing facility | $10,000.00 | 1.20% – 1.55% | 5 or 7 years | See “Key Feature? | None | A+ |

| Global Atlantic ForeIncome II | Fixed Indexed Growth | Deferred | Guaranteed Income Builder Benefit offers a steady, predictable income for your entire life. | $25,000.00 | Linked to S&P | 5, 7, or 10 years | Free – up to 10% of contract value after 6 years | None | A |

| Lincoln Financial OptiBlend | Fixed Indexed Growth | Deferred | Performance of portfolio is tied to the performance of four different indexed accounts | $10,000.00 | 1.90% on premium amounts of $100,000 – $2,000,000 | 5, 7, or 10 years | Free – up to 10% of contract value | None | A+ |

| Sentinel Security Life | Multi-year Guaranteed | Deferred | If you become terminally ill or nursing home care withdrawal charges are waived. | $2,500.00 | 3.20% | 10 years | None | B++ | |

| Atlantic Coast Life Insurance | Multi-year Guaranteed | Deferred | A favorable rate that’s higher then financial products like CDs. | $2,500.00 | 3.30% | 10 years | None | B++ | |

| Canvas Annuity Future Fund | Multi-year Guaranteed | Deferred | Accessibility. Anyone over age 18 can apply. And, you can access your account 24/7 | $2,500.00 | 3.30% | 20 years | None | B++ | |

| Oceanview Life Harbourview MYGAs | Multi-year Guaranteed | Deferred | Market value advisement, as well as expansive age range from 0 to 89 | $20,000.00 | 3.25% | 7 years | Free – up to 10% of contract value | None | A- |

| Nassau Simple Annuity | Multi-year Guaranteed | Deferred | Single-premium, multi-year guaranteed annuity that offers protection from market volatility | $5,000.00 | 3.10% | 3, 4, 5, 6, 7 & 10 years | Free – up to 10% of contract value | None | B+ |

| Fidelity Personal Retirement Annuity | Variable | Both | Offers three different investment styles; hands-on, hands-off, sector investing. | $10,000.00 | – | 6 years | Free – up to 5% of your contract value | None | A- |

| Jackson National Life Perspective II | Variable | Deferred | Highly customizable with a max annuization age of 95 | $5,000.00 | – | – | Free – up to 10% of contract value | 0.25% for contracts purchased with an initial investment of less than $1 million (or which have not yet accumulated $1 million) | A |

| Transamerica Life Principium IV | Variable | Deferred | Back to basics with an investment only strategy | $1,000.00 | – | 7 years | Free – up to 10% of contract value | $35 | A |

| MassMutual Transitions Select II | Variable | Deferred | Choose sub accounts that are managed by Oppenheimer Funds and Franklin Templeton Investments. | $10,000.00 | – | – | Free – up to 10% of contract value | $40 | A++ |

| Brighthouse Financial Variable Annuities with FlexChoice Access | Variable | Both | Receive 5% compounding and Automatic Step-Ups | $10,000.00 | – | – | Free – up to 10% of contract value | $30 | A |

| Athene Amplify | Registered Index | Both | Four different index options. | $10,000.00 | 1, 2, or 6 years | Free – up to 10% of contract value | $30 | A | |

| Equitable Structured Capital Strategies | Registered Index | Both | Customizable and levels of downside protection that are up to -30% | $25,000.00 | Free – up to 10% of contract value | 1.15% variable investment option fee | A | ||

| Allianz Index Advantage | Registered Index | Both | Ability to subscribe to a specific type of index strategy through the company. | $10,000.00 | Free – up to 10% of contract value | 1.25% annual product fee | A+ | ||

| Nationwide Monument Advisor | Registered Index | Both | The industry’s first flat fee, Investment Only Variable Annuity (IOV) | $15,000.00 | Free – up to 10% of contract value | $20 | A+ | ||

| Prudential FlexGuard Indexed Variable Annuity | Registered Index | Both | Provides a guaranteed income stream with ability to choose buffer level | $25,000.00 | 1, 3, or 6 years | Free – up to 10% of contract value | None | A+ |

Methodology

In order to determine the best annuity rates for each category, we considered the costs and benefits of each annuity on the market. Costs of each annuity include: the annual fee, withdraw transaction fee and the annuity rate offered by the annuity company. Benefits and perks are different for each person. Initial contribution minimums tends also be a large contributing factors in your purchasing or not purchasing.

In addition, each annuities category has its own criteria. For fixed annuity rates we also considered how much value you can expect to get guaranteed over the volatility in a variable or indexed annuity rate. We find fixed annuity rates range from 1% to 3%. Variable and Indexed tend to be from -2% to 6% interest on your money. This was a large factor in which annuity rate has the lowest net cost.

For annuities meant for those who are trying to build long term retirement or have 15+ years till retirement, we focused on annuity offers that offer the most opportunities to have a sustainable rate over the longest period of time with lowest net cost to the consumer.

For indexed annuities we looked at the length of variable rate, minimum initial premium and fees.

Every A.M. Best Rating was factored when comparing which annuity rate is the best.

Other Annuity Facts To Be Considered

10 Steps to Take Now for a Tax-Free Retirement

“Our new Constitution is now established, and has an appearance that promises permanency; but in this world, nothing can be said to be certain, except death and taxes,” Benjamin Franklin wrote in a 1789 letter.

The significance between that often-cited quotation? It’s often the first attribution to the adage, “Nothing is certain except for death and taxes.”

Steps to Take Now for a Tax-Free Retirement

However, The Yale Book of Quotations quotes “‘Tis impossible to be sure of anything but Death and Taxes,” from Christopher Bullock, The Cobler of Preston (1716). And, also it quotes “Death and Taxes, they are certain,” from Edward Ward, The Dancing Devils (1724).

Regardless of its origins, that adage is arguably one of the most honest statements about life. And, yes. Even while enjoying your Golden Years, you still have to worry about the taxes.

In a way, that kind of seems unfair. I mean, you’ve paid your dues. Now it’s time to enjoy the fruits of your labor. But, you know. Life sometimes just isn’t fair.

Estimating your taxes in retirement.

Now that I’ve ripped the band-aid off and you know that you’ll have to pay taxes, how exactly are they calculated?

Well, they’re based on your income — just like your pre-retirement days. However, different rules apply to the various retirement income streams that you’ll receive.

Here are the most common types of retirement income and the rules that are attached to each.

Social Security income.

If this is your sole source of income, then you don’t have to pay taxes. But, what if you have other sources of income? When you file a return, you might have to include up to 85% of your benefits as taxable income.

Thankfully, the IRS has a handy tax worksheet to help you determine how much your benefits will be taxed.

IRA and 401(k) withdrawals.

The good news? Generally, Roth IRA distributions are tax-free. The reason is simply that you paid taxes on this money upfront.

That’s not the case with tax-deferred retirement accounts. These include 401(k) plans, 403(b) plans, and 457 plans, as well as traditional IRAs.

Why? Well, since they’re tax-deferred, that means you must report withdrawals from these plans on your tax return as taxable income.

Just note that the amount of tax will depend on a couple of factors—namely, the total amount of income and deductions you have. And what tax bracket you’re in.

Pension income and annuity distributions.

According to the IRS, “If you receive pension or annuity payments before age 59½, you may be subject to an additional 10% tax on early distributions, unless the distribution qualifies for an exception.”

“The additional tax generally doesn’t apply to any part of a distribution that’s tax-free or to any of the following types of distributions:”

- That was “made as a part of a series of substantially equal periodic payments that begins after your separation from service.”

- You “made because you’re totally and permanently disabled.”

- They were “made on or after the death of the plan participant or contract holder.”

- You “made after your separation from service and in or after the year you reached age 55.

- That is “up to $5,000 made within a year of the birth or adoption of your child to cover birth or adoption expenses.”

One way to avoid paying taxes on your pension income is to have your taxes withheld directly from your pension check.

Also, the interest portion of your annuity will be included in your taxable income. You’ll also pay taxes on earnings or investment gains.

Investments income.

Just like you did before retiring, you’re going to have to pay taxes on capital gains, dividends, and interest income. Any income you’ve earned from investments will be reported on a 1099 tax form each year. And, the financial institution that holds these accounts will send you this form directly.

What if you’re selling investments to generate a retirement income? You must report this on your taxes.

If you have a mature CD in the amount of $10,000, it’s not considered taxable income.

Gains when selling your home.

As long as you’ve lived in your home for at least two years and you have gains less than $250,000 if you’re single ($500,000 if you’re married), then you won’t have to pay taxes on selling your home. It does get tricky when you’re selling a home that you’ve rented out.

How can you calculate your tax rate?

Well, this will depend on the sources and income. Generally, you’ll want to list all of your retirement income and add that up. Next, you’ll reduce that by the deductions that you anticipate for the year.

You can enter this information into your tax software program. Or, you can save yourself the hassle and pass it along to your accountant.

But, I have some good news for you. You can minimize retirement taxes if you take the following steps.

1. Know your tax bracket.

If you want to reduce your tax burden or possibly enjoy a tax-free retirement, then this is the absolute first step you must take.

How exactly do tax brackets work? Well, in the States, we have something called a progressive tax system. Tina Orem over NerdWallet explains that this means those “with higher taxable incomes pay higher federal income tax rates.”

However, there are a couple of caveats to be aware of.

- “Being ‘in’ a tax bracket doesn’t mean you pay that federal income tax rate on everything you make,” adds Orem.

- “The government decides how much tax you owe by dividing your taxable income into chunks — also known as tax brackets — and each chunk gets taxed at the corresponding tax rate.”

In both 2020 and 2021, there were seven federal brackets; : 10%, 12%, 22%, 24%, 32%, 35% and 37%. Each depends on your taxable income and filing status.

So, here’s how this could be applied to you;

- You will owe 10% of taxable income if you make $0 to $9,875.

- Do you make $9,876 to $40,125 ($19,751 to $80,250 for couples)? If so, you’ll owe $987.50 plus 12% of the amount over $9,875. For joint filers, this would be $0 to $19,750

- You would fall into the 22% if you made $40,126 to $85,525 and $80,251 to $171,050 for joint filers. As such, you would owe $4,617.50 plus 22% of the amount over $40,125.

- If you earned $85,526 to $163,300 if single and $171,051 to $326,600 if married then you’ll have to pay $14,605.50 plus 24% of the amount over $85,525 in taxes.

- You’ll owe $33,271.50 plus 32% of the amount over $163,300 if you had income between $163,301 to $207,350 (single) and $326,601 to $414,700 (couples)

- For those earning $207,351 to $518,400 ($414,701 to $622,050 if filing jointly), you’re on the hook for $47,367.50 plus 35% of the amount over $207,350.

- If you raked in $518,401 or more (single) and $622,051 plus for couples, then you’ll owe $156,235 plus 37% of the amount over $518,400.

One way to avoid paying more in taxes than you have to, and you have both traditional and Roth accounts, then limit your traditional account withdrawals. This will ensure that you won’t be taxed at a higher marginal rate. After that, supplement that retirement income as needed with tax-free withdrawals, such as from a Roth account.

2. Asset location.

“Financial advisors generally encourage account diversification among clients — meaning, having some savings in a taxable account, a traditional (pre-tax) 401(k) or individual retirement account, and a Roth 401(k) or IRA,” writes Greg Iacurci for CNBC.

As a result, investors have more flexibility when withdrawing funds.

“Investors can maximize their tax savings by holding certain investments and funds in the appropriate type of account,” he adds. Known as “asset location,” this “boosts an investor’s after-tax rate of return.”

“For example, investors should generally consider holding stocks and stock funds in taxable accounts,” says Iacurci. “These investments are more ‘tax-efficient — meaning most of their return is from capital gains taxed at a rate that’s less than ordinary income.”

“On the other hand, investors should generally hold bonds and bond funds in retirement accounts,” Iacurci advises. “These investments are less tax-efficient since most of their returns are dividends taxed as ordinary income.”

So, let’s say that you’re an investor with a grand in a taxable account and another $1,000 in a 401(k) and want “a 50-50 stock-to-bond allocation.”

“Holding $1,000 of stocks in the taxable account and $1,000 of bonds in the retirement account (instead of doing a 50-50 stock-bond split in each account type) would generally be the most tax-efficient approach,” he states.

3. Diversity your tax liability.

“When looking at your retirement savings, it’s important to consider the types of accounts you’re saving and investing in. Tax-deferred accounts,” recommends Tony Drake, CFP®. Examples include a 401(k) and traditional IRA. These “offer tax advantages now” since you “contribute money before taxes.” However, you’ll still owe the IRS when you make a withdrawal.

“Tax-exempt accounts, like a Roth IRA or Roth 401(k), offer tax advantages in the future,” adds Drake. “Your money is taxed before you contribute to the account, but you can withdraw it tax-free in retirement.”

You should also consider taxable accounts, such as brokerage and savings accounts. You’re “taxed on the interest you earn and on any dividends or gains,” he says. “Investment accounts are an important part of your overall financial plan, especially during your working years as you grow and accumulate your savings for retirement.”

“How much you contribute to your retirement accounts during your working years and the types of accounts you contribute to will impact how much you pay in taxes both now and in retirement,” Drake adds. “Diversifying your savings and investment accounts will help you better control your tax situation in retirement; you gain more flexibility on how much you withdraw and from which account.”

4. Catch-up on contributions.

Once you hit age 50, you’re eligible for an additional tax break if you make catch-up contributions. For 2020 and 2021, you’re permitted to defer taxes on an additional $6,500 in a 401(k) and $1,000 in an IRA.

5. Make tax-exempt investments.

In addition to 401(k)/403(b) employer-sponsored retirement plans and IRAs, here some other tax-free investments you should throw money at;

- Health Savings Account (HSA)

- Municipal Bonds

- Tax-free Exchange Traded Funds (ETF)

- U.S. Series I Savings Bond

- Bonus: Indexed Universal Life Insurance

- Charitable Donations/Gifting

- 529 Education Fund

- 1031 Exchanges

6. take advantage of the saver’s credit.

Have you earned up to $32,500 and you’re single? What if you’re a couple with $65,000 set aside?

You can make contributions to your 401(k) or IRA using the saver’s credit. If you take advantage of this, you can either increase your refund or reduce the tax owed. How much? It could be as much as $1,000 for individuals and $2,000 for couples.

7. Watch your timing.

A surefire way to pay the lowest amount of taxes throughout your retirement is to maintain a level of income. Why? Because if your income was low this year, but high next, then you will end up paying more in taxes.

In other words, you want your withdrawals and selling of assets to be steady. For instance, if you sold capital assets at a loss, you might want to unload other assets that performed well to offset your capital gains.

Another suggestion? If you have more income from earnings, assets sales, or other taxable income in one year, then wait to withdraw money from traditional retirement plans until December 31.

8. Be strategic about Social Security benefits.

If you don’t need your Social Security benefits, then pushback receiving this benefit until after 70. The reason being is that you’ll earn additional credits, which will increase your monthly benefits. You also don’t have to worry about paying taxes on Social Security right now.

Once you receive these benefits, they’ll either fully tax-free or are included in your gross income at 50% or 85%. It just depends on your income.

Just know that if your provisional income, which is the taxable portion of your Social Security benefits, is below $25,000 and you’re single, your benefits won’t be taxed. For those who filed jointly, this would come out to $32,000.

9. Relocate to a tax-friendly state.

If you don’t already reside in a tax-friendly state, consider relocating to Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington, or Wyoming. These states don’t have income taxes.

New Hampshire taxes only interest and dividends. Meanwhile, Illinois, Mississippi, and Pennsylvania don’t tax distributions from 401(k) plans, IRAs, or pensions. And Alabama and Hawaii don’t tax pensions but still tax distributions from 401(k) plans and IRAs.

Thanks to the Tax Cuts and Jobs Act, this is particularly important as just $10,000 in local property, state and local income, or sales taxes can be deducted for federal income tax purposes.

Also, federal law bars taxing residents on retirement benefits that were earned in another state. So, if you want to pack up and leave high-tax states like New York or California, you can still move to a no-tax state and still collect your pension tax-free.

10. Remember required minimum distributions.

A required minimum distribution, RMD, is the required minimum amount of money that you must withdraw from a tax-deferred employer-sponsored retirement plan. These include most 401(k)s and IRA. And, it occurs when you reach age 72 — or if you turned 70½ in 2019.

If you don’t comply, the IRS will slap you with a hefty penalty fee, usually taxed at 50%.

To ease this burden, consider;

And, finally, make sure that you work with a financial advisor so that you are taking the right and legal steps to enjoy a tax-free retirement.

Understanding Your New Investment Accounts

How do you know what new investment accounts you should open when you’re a beginner? Investing is a topic that many find stressful. Especially when you are just getting started. There is always the advice of “talk to a financial advisor!” but when advisors are often looking for clients that have a minimum of $250,000 of investable assets that they can charge 1% on, is that always a feasible choice? As someone who used to be a financial advisor, I’d like to say that investing without a financial advisor has actually never been easier.

Big, well-known firms have all dropped trading fees to $0 to compete for your business. New companies are opening that are strictly online or on mobile apps. Account balances and your net worth update instantly. We can literally handle all of our finances on the rectangle that fits in our pocket!

It’s easy to get overwhelmed with all of the options available. So, what investment accounts should beginners look at opening first?

The before-you-invest account

Whether you are a beginner to investment accounts or not, you should make sure to have one account checked off before starting. An emergency fund. How big your emergency fund needs to be is up to you and your needs, but there should be some savings set aside for the inevitable.

When you are investing your money, it is no longer “liquid”. This means it is more difficult to pull out cash to buy an item or pay for an expense. It’s not impossible- it just takes the transaction time of selling your investment position, then moving the cash from your investment account to your checking account. This process can take several days and may incur taxes along the way, depending on which account the money is taken from.

To avoid unnecessary taxes or potentially selling your positions at a loss, you should have an emergency fund in place to cover expenses that pop up. Yes, your investment accounts are there, and your money if you need it, but they should not be your first line of defense!

Two Types of Investment Accounts

There are many, many different investment account options out there. However, all of the different accounts you see can really boil down into two categories. Those categories are retirement and non-retirement.

One big mistake beginners make with investing is thinking they are too young to worry about saving for retirement. But investing and retirement planning actually go hand-in-hand! Investing is a tool to build wealth. Retirement is an inevitable phase of life that requires wealth.

To make the most out of your investing experience, you should start saving for both short and long-term goals. While retirement is a crucial thing to be saving for, it’s not normally your only financial goal. There are inevitable expenses in the short to medium term that investing can also help fund.

Understanding the type of account that will best fit your goals is key. Then, knowing that life will throw you all types of expenses, put your investments to work to help fund them.

Retirement Accounts

You should understand that ‘retirement accounts’ is actually a huge umbrella! While they all have the same objective: money saved for your future, their ways to get there are all different. Each account has a slightly different set of rules, limitations, and tax situations. This is why you might be more comfortable talking to a financial or tax advisor about your unique situation.

Start investing in your 401k or 403b

The first investment account that beginners should consider is, hands-down, a 401k or 403b through an employer. This is because of ease of entry, not because of any other investing perks! If you don’t have an employer 401k or 403b through work, don’t panic. There are still plenty of great investment account options for you.

If you do have access to a retirement plan at work, use it! Saving your money can be a difficult habit to get into. It will make saving a whole lot easier when a portion can automatically be taken from your paycheck.

Money that is coming directly from your paycheck also gets the perk of not being taxed. Your 401k or 403b contributions get deducted from your taxable income when you file your taxes. This means your seeing some tax savings on your saved money!

What about the “employer match”?

An “employer match” is a deal you don’t want to leave on the table. This is money that your employer will put into your account, for free, based on an amount you are putting in. It’s common to hear of employer matching of 3-6%, but I’ve witnessed matches as high as 10%. Yeah, I was jealous too.

This percentage could be based on your income, or it could be based on a dollar amount you contribute. But, regardless of the formula, you don’t get the match unless you are also contributing to your account!

Ask questions about employer matches and keep asking questions until you understand how it works! In the best-case scenario, you should be shooting to contribute enough to get the full employer match that’s available.

How to start investing when you don’t have a 401k

While saving in a 401k and employer matching is nice, not everyone has access to it. If you don’t have a 401k or 403b option at work, you’re going to have to be a little more involved in your finances. This is not a bad thing! This means you have a LOT more freedom as far as your investment options. Having access to all options means you can choose investments with lower fees, which is a common complaint in 401k and 403b plans.

For those that don’t have employer plans, or for those that do but who want to be doing more saving, there are Individual Retirement Accounts, or IRA’s. Make sure you understand the IRS’s rules on these accounts! While there are perks, there are also limitations. The most common one is not being able to withdraw your savings until age 59.5, the deemed “retirement age”.

These accounts can be invested, just like employer plans. Being able to invest inside your retirement account is the key ingredient to having enough money to retire.

IRAs beginners should start with

The first investment accounts beginners without 401k’s should consider are the Traditional and Roth IRA. These accounts can be funded up by anyone with earned income, which is income from a job or self-employment. Things that don’t qualify as earned income are interest, dividends, alimony, child support, and social security.

Opening up a traditional or Roth IRA is not difficult, and it isn’t something that should intimidate you! You open your account with a custodian, like Vanguard, Fidelity, or Charles Schwab. Most custodians offer free account opening, no minimums, and free trading. Most accounts can be opened online, in less than 15 minutes. Remember when I said investing without an advisor has never been easier?

Traditional or Roth IRA?

Should you start investing in a traditional or Roth IRA? This is one of the biggest questions for new investors. Both accounts will help you save for your retirement years, but they have a very big difference when it comes to how they are taxed.

When you are saving in a traditional IRA your contributions will be deducted from your taxable income. This is how 401k’s and 403b’s work as well. When you put money into your traditional IRA, it will get subtracted from your income when you file your taxes. This makes the amount of money you owe taxes on smaller, and gives you tax savings today. For those who are looking to replace not having a 401k at work- the traditional IRA is a closer comparison.

Note: there are Roth 401k and 403b’s that exist, to which the above does not apply!

The Roth IRA works differently. In the Roth IRA, you do not deduct your contributions when you do your taxes. This means you are not taking any tax savings today. Instead, you most likely already paid income taxes on the money that went in. I know, this doesn’t seem like a great tax perk right now, but bear with me…

Taxes on withdrawals

There are key differences to these accounts when you are withdrawing money from your IRA. This is when the Roth IRA’s perks begin to show! Because you already paid taxes on the money you put into your Roth IRA, in the IRS’s eyes, you’re done paying taxes. Your entire account balance is yours. Imagine… 20, 30, 40, 50 years down the road when you are withdrawing your money from these accounts. Now imagine never having to worry about paying taxes on it. Doesn’t that make you want to plan your retirement vacations right now?

The traditional IRA had better tax perks in our saving years, but now, they aren’t looking as nice. In the traditional IRA, since you were deducting your contributions, you technically haven’t paid any taxes yet. The money you withdraw from traditional IRA’s get taxed as income. This means you will have to pay income taxes on every single withdrawal. How much in taxes? Well, that depends on whatever tax system you’re in at that time.

Many people agree that already paying their taxes provides a special peace of mind. Especially for those who think taxes will increase in the future. This makes the Roth IRA a favorite for many. However, you will want to make sure you do not exceed the annual income threshold for making contributions.

It’s likely you will need to use both accounts in your lifetime, so don’t get hung up on which is “better”. If you are just beginning in one of these investment accounts, getting started is the important part.

Traditional and Roth Annual Limits

The annual limit for contributions to these accounts in 2020 and 2021 is $6,000 or $7,000 if you are over age 50. Note that is the combined limit, not individually! If you put $6,000/$7,000 in a Roth IRA in a given year, you could not put any in a Traditional IRA that same year. You could put $3,000 in each, or any combination that adds up to the limit, but not more than.

This is an area where 401k’s and 403b’s show more benefit. The annual contribution for those accounts is much higher at $19,500. People trying to save a significant amount for retirement are capped by the much smaller limit of the traditional and Roth in comparison.

However, those just getting started might benefit from a lower annual limit, as it makes a great goal. Having a $6,000 max on this investment account when you’re a beginner could mean setting an investment goal of $500 a month. This would max out an account, and could add up to a large sum of money by retirement time!

Other IRA Options

When you are self-employed there are even more IRA options for you to start investing. But if you don’t expect to be investing more than $6,000 a year, there is nothing wrong with sticking with the Traditional or Roth.

If you are hoping to put away more than that for your future, you should consider opening a SEP or SIMPLE IRA. Which one you choose will depend on your business and the number of employees.

When you are a beginner to investment accounts, don’t feel like you need to open multiple IRA’s at once! Decide which one makes the most sense for your current situation. You might want to read more about the differences in tax perks and see which account is most useful given your current situation.

Non-Retirement Accounts

Once you have some money being regularly invested for your future, you should consider other financial goals. If you know you have big expenses coming up in the next 5-20 years, things like homes, weddings, or college tuition, investing could help you out. But keep in mind, It’s not a good idea to start investing for short-term goals. The market could be down when you are in need of your funds, and you could risk having less money than you put in. The longer the time-frame, the greater your chances of a balanced out, positive return.

Setting up non-retirement investment accounts can also prevent you from tapping into retirement funds early if you need money for an emergency. This is also why you should have an emergency fund established before you start investing.

Non-retirement investment accounts do not see the same tax savings as retirement accounts. You will not write off any of the money you put in, and when you sell out of a position, you will owe taxes on any gains. You should get familiar with short-term and long-term capital gains taxes when you are investing in these accounts. Always consult a financial or tax professional if you are unsure about your tax situation!

Individual brokerage accounts

This is probably the most common investment account in the non-retirement category. Beginners who opened investment accounts through apps like Robinhood and Acorns most likely opened up an individual brokerage account. As the title suggests, this account is for individuals, so only one person can be listed on the account.

Again, the biggest perk is inside this account is being able to invest. Unlike money in your savings account, you can invest the cash you move to these accounts into companies or commodities. You can buy stocks, exchange-traded funds, mutual funds, index funds, and more. There is no guarantee your money will grow. Remember, you should always be doing your own research before you start investing, and understand the risks involved.

You should also be aware of the tax happenings inside of your new investment account. You will pay short-term capital gains tax on positions held for less than a year. If you hold your position for over a year, you will be taxed at the lesser, long-term capital gains tax rate.

Don’t let tax fears prevent you from starting your investing journey! Your custodian will send you tax forms in January or February with any tax information you’ll need for filing your taxes. You only owe taxes on the growth of your money. Paying taxes on your growth is better than not growing at all!

Joint brokerage accounts

If you have a spouse, you might be considering a joint brokerage account for your money goals. You can open joint accounts with non-spouses too, just use caution, as both account owners will have full access! Joint accounts might be considered for business partners or family members, just make sure all of the terms are understood by all parties.

Joint brokerage accounts are treated the same as individual accounts, except they allow more than one account owner. You should anticipate the same investment options and tax rules when it comes to this account!